Something’s brewing.

We don’t know what it is, but it feels ominous. It could just be bias playing with our mind. That is, we know the financial system is broken and that the market should collapse. We know you can’t solve a debt problem by increasing debt.

So we wait for something to happen.

Markets have conveniently settled down over the latter part of the northern summer. The power-brokers and money-managers have gone to the beach. It’s all going to script.

It’s probably no coincidence that as soon as the politicians get out of everyone’s way calm returns to the market. There’s no one around to stuff things up!

But things are already stuffed up. It’s the rate of decay that’s important. The rate usually slows down in the northern summer (although it didn’t in 2011) and speeds up in the volatile September and October period. Things may have been eerily quiet recently, but remember, there are just two weeks left in August…

Jim Rickards, who presented at our Strategy Session on Tuesday, reckons the most likely outcome of all this is chaos. He wasn’t trying to be alarmist. He’s just saying that when a system of international finance comes to an end, it normally goes through a chaotic period before another system emerges.

What will that system be? Rickards puts a number of options forward. All involve something taking over from the US dollar as the world’s reserve currency. The problem with the US dollar is that it fulfils the dual role of domestic currency and international reserve asset. This gives rise to the ‘Triffen Dilemma’, named after the US economist Robert Triffen. The dilemma is that the objectives of managing a domestic currency run contrary to the objectives of an international reserve asset.

For example, the US runs a trade deficit. It has done for decades. US trade deficits supply global liquidity. Excess US dollars flow to Middle Eastern oil producers, Chinese widget manufacturers and Japanese car makers.

What do you think would happen if the US suddenly became competitive and financially prudent? What if it started producing trade surpluses? It would be disastrous for the global economy. Global liquidity would dry up…there would be a massive credit crunch.

So the system depends on US profligacy. The US may enjoy an ‘exorbitant privilege’ in the words of former French President Charles De Gaulle , but it’s one that has benefitted – and we use that term loosely – the world in terms of delivering debt-based economic growth.

But for how much longer? Triffen identified the problem way back in the 1960s. Since then nothing has changed. The dilemma is now so big that it can’t be undone or reversed. The dual role of the US dollar as national and international currency is no longer viable.

So what happens next? Well, we can guarantee that any change will not be smooth or voluntary. The maintenance of the ‘system’ has many powerful beneficiaries. Which is why they’ll hold on until the death before change forces itself upon us.

Rickards reckons the IMF (international Monetary Fund) could come in and produce SDRs, or special drawing rights. SDRs are effectively a unit of account defined by the value of a basket of currencies: the US dollar, the euro, the British pound, and the Japanese yen.

These SDR’s could replace the international reserve role of the US dollar and in part solve Triffen’s Dilemma. But is issuing a piece of paper, backed by other pieces of paper and managed by a bunch of policymakers, a better system than the one we’ve got? Are SDRs relevant if it’s the ‘old’ industrial, debt-soaked powers who ultimately stand behind them?

Probably not. But the elites who run the system are from the old, debt soaked industrial powers, and they’ll do anything to keep their hold on power. This is why having SDR’s as a reserve currency is probably more realistic than you may think.

Would it be easy for the IMF to introduce SDRs? After all, their use means all international trade would be denominated in the SDR unit of account. Somehow we think getting international agreement on this will be difficult. But in times of chaos, obtaining agreement on something for the benefit of the few is not so difficult. The fear of the unknown and even greater chaos weakens democracy. We’ve seen it happen in Europe.

The other option Rickards came up with was gold as the replacement for the US dollar. However, he says this has no official support. He reckons there is no central banker around who supports a return to gold…which is reason enough for the rest of us to support it.

But a new system doesn’t necessarily have to have official support. It can just evolve organically. If each participant in this economic system, large or small, realises that a portion of their wealth is best protected by the physical ownership of gold, then gold will automatically assume a major role to play in the new financial system.

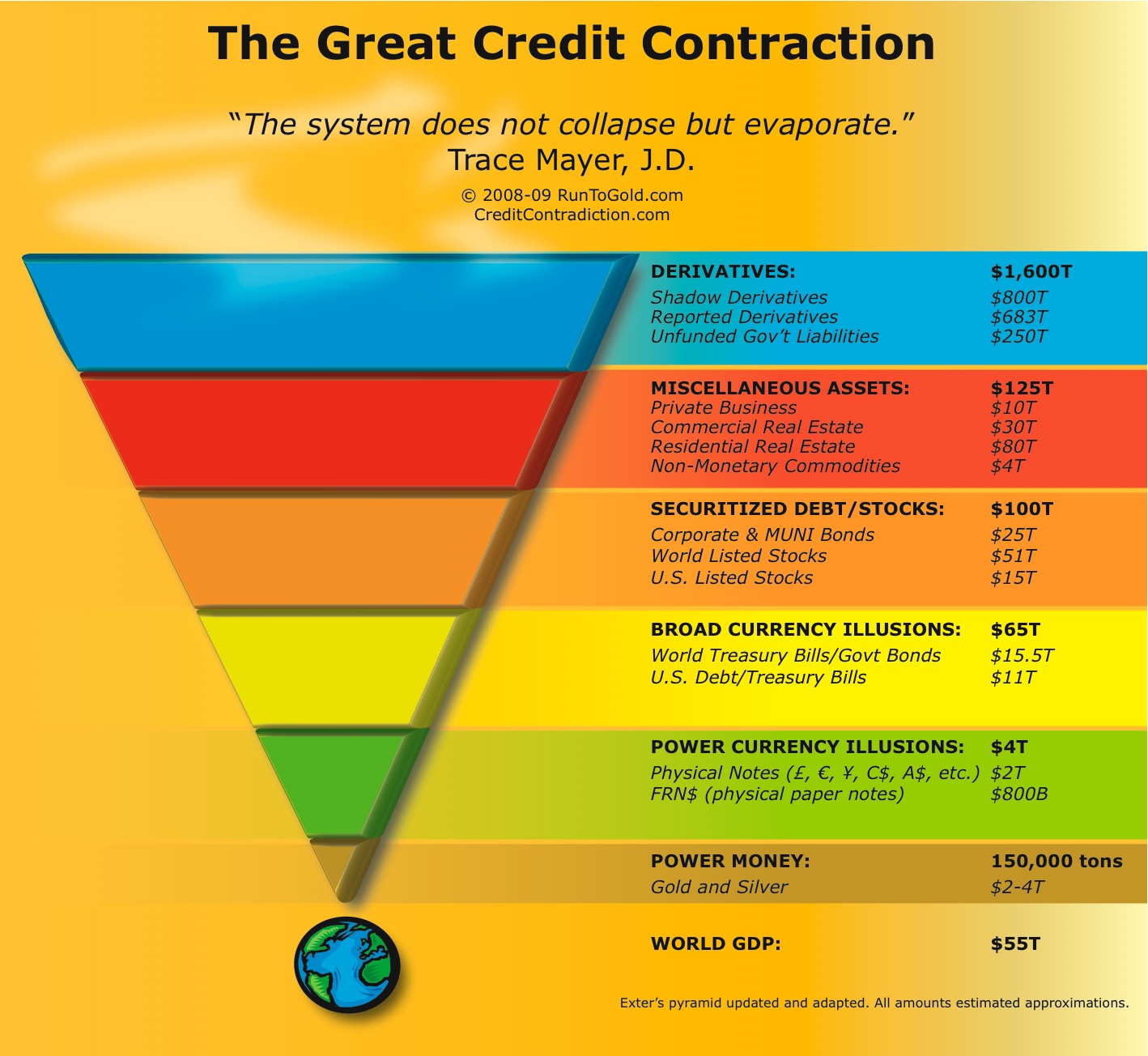

Rickards gave a few examples of what the future price of gold might look like based on various monetary aggregates. Using US M2 money supply and the US gold stock of just over 8,000 tonnes gives a gold price of US$30,862 per ounce. Assuming 40% backing of the money supply gets you to a $12,347 per ounce price.

These are just estimates of course. But even Rickards’ lowest estimate, at 40% of M1 money supply, produces a gold price around US$2,600. That’s well above the current price of gold. But gold is a market currently dominated by paper based gold derivative trading. We’ve shown before how the volumes traded on the over-the-counter market in London dwarf the estimated available physical supply.

Clearly, gold trading works like fractional reserve bank lending. This goes unnoticed in a financial system functioning smoothly. But it starts to break down when trust in the system breaks down. That’s because gold has no counterparty risk. It can’t default and can’t go bankrupt. Gold becomes more valuable as the system deteriorates.

And as the system deteriorates, gold flees, making fractional-based gold trading more and more difficult.

Our money is on an organic system of finance evolving out of the old, US dollar debt-based system. We’ll call it ‘organic finance’. It will involve gold priced at much higher levels than it is now. That’s because the gold price has nowhere near kept up with the explosion in global credit in the last 40 years.

And because authorities refuse to restructure or write-off bad debt monetising that debt slowly is the only alternative.

That in itself will cause a whole bunch of other problems. We’ll look at what they might be tomorrow.

Regards,

Greg Canavan

for The Daily Reckoning Australia

FOFOA

FOFOA

{kind=link}