Another amazing essay from FOFOA. As always, I highly recommend reading FOFOA extensively. His concept of FreeGold is the end game IMO.

The Shoeshine Boy

To set up this post I will share with you two brief predictions I recently received by email. These were both in email blind copied to large groups of recipients that included me. The two senders do not know each other. In fact, their only connection is that they are both supporters of my blog on the highest order, I know what they each do for a living (very respectable), and I therefore hold them both in high regard:

Email 1:

This is a very orderly secular bull market. The bubble, that WILL come, is still about 2 or 3 inches to the right of the margin on the right side of this chart…

Email 2:

Perhaps we are talking about the first general realization among the investing public that the Fed cannot/will not rescue us with their magic wands and QEs… This may be it, the beginning of Stage 2 of gold’s rally, where the smart money starts moving in. Stage 3 is next when the shoeshine boy tells you: Buy gold!

For those of you that don’t know the meaning of the shoeshine boy reference, JFK’s father, Joe Kennedy claimed that he knew it was time to get out of stocks in 1929 when he received investing tips from a shoeshine boy. Ever since, the shoeshine boy has been the metaphor for “time to get out”; for the end of the mania phase in which everyone, even the shoeshine boy, wants in.

Joe Kennedy

Joe Kennedy’s credibility on this “bubble top calling” issue is bolstered by the fact that from 1929 to 1935 his fortune went from $50 million to $2.85 Billion in today’s purchasing power. And the take-home lesson in this story is that it is time to sell ANYTHING once the shoeshine boy is recommending it. Because the next phase is the blow off phase where the item in question comes crashing back down.

Bubble Phases

And the fact that two of my favorite readers are now calling for an eventual bubble in gold reminded me that it has been 9 ½ months since I wrote Gold: The Ultimate Un-Bubble. Perhaps it is time for an update.

Now I’ll grant that the point in both of the quotes above was that we are nowhere near the bubble top. And they were addressed to people that are very jumpy when it comes to bubbles because they have been burned by a couple bubbles in recent history. But even so, I think they expose a fundamental misunderstanding of what is actually happening today.

How Gold will handle even the Shoeshine Boy

Before I get into what is actually happening with gold today, I want to show you WHY it is happening to gold. And WHY gold is different. There’s a unique thing that happens with gold. ANOTHER said it pretty clearly (even if still a bit cryptic) in his very first post:

“Gold has always been funny in that way. So many people worldwide think of it as money, it tends to dry up as the price rises.”

In a future post I’ll explain the context in which ANOTHER made this statement because it portends vast changes in the international monetary system directly in front of us. (Remind me of this. I was going to include it here but the post grew too long even without it. 🙂 But for now, we need to look at why this statement is true. For this I turn to John Law. Well, not the real John Law, but another pseudonymous blogger like me using his name back in 2006:

An illustration

Let’s start by comparing two hypothetical cases.

In case A, a million Americans decide right now to move all their savings into Dell stock, buying at the current market price no matter how high.

In case B, a million Americans decide right now to move all their savings into gold, buying at the current market price no matter how high.

In both cases, let’s say each of these test investors has an average of $10,000 in savings. So we are moving $10 billion.

Neither gold nor Dell can instantly absorb $10 billion without considerable short-term increases in price. Because it would require us to predict precisely how other investors would react, we have no way to precisely compute the effects. But we can describe them in general terms.

In case A, the conventional wisdom is right. Our test investors should expect to lose a lot of money.

This is because Dell has a stable equilibrium price which is set by the market’s estimate of the future earning power (price-to-earnings ratio) of this fine corporation. Because it is not the result of any new information about Dell’s business, the short-term surge should not affect this long-term equilibrium.

Since there will almost certainly be a short-term price spike, many of the test investors will be buying at prices well above the stable equilibrium. In fact, the more investors we add to the test, the more each one should expect to lose. Doh!

But there is no way to apply this analysis to case B.

Precious metals have no price-to-earnings ratio. With gold formally demonetized (that is, with no formal link between gold prices and currencies such as the dollar, as there was until 1971), there is no stable way to price it. There is no obvious equilibrium to which the gold price must converge.

It is true that gold has industrial uses. It can be priced on the basis of industrial supply and demand. The conventional wisdom is that it is.

Thus we can say that gold, for example, is overvalued if gold miners are selling more gold than jewelry makers and other industrial users want to buy. At present (with gold near $700), they probably are. So if you follow this reasoning, the right investing decision is not to buy gold, but to sell it short.

But this just assumes that there is no investment demand for gold. On the basis of this assumption, it shows that gold is a bad investment. Therefore there should be no demand for it.

Therefore, when our case B investors put $10 billion into gold, that money has to be used to bid gold away from its current owners, many of whom already believe that the price of gold in dollars should be much higher than it is now.

So the result of case B is that the gold price will, as in case A, rise immediately. But it has no reason to fall back.

In fact, quite the opposite. Because the gold price is largely determined by investment demand, any increase in price is evidence of increasing investment demand. Mining production, noninvestment jewelry demand, and industrial use are relatively stable. Investment demand is a consequence of investors’ opinion about the future price of gold – which is, as we’ve just noted, largely determined by investment demand.

This is not a circularity. It is a feedback loop. Austrian economists might call it a Misesian regression spiral.

Suppose you believe this. It’s all well and good. But what does it really prove? Couldn’t gold still be just another bubble?

And why should gold be a better investment because it has no earnings to price it by? This makes zero sense.

To answer these sensible objections, we need a few more tools.

Nash equilibrium analysis

The Nash equilibrium is one of the simplest and oldest concepts in game theory. (Nash is John Nash of A Beautiful Mind fame.)

In game theory jargon, a “game” is any activity in which players can win or lose – such as, of course, financial markets. And a “strategy” is just the player’s process for making decisions.

A strategy for any game is a “Nash equilibrium” if, when every player in the game follows the same strategy, no player can get better results by switching to a different strategy.

If you think about it for a moment, it should be fairly obvious that any market will tend to stabilize at a Nash equilibrium.

For example, pricing stocks and bonds by their expected future return (the standard Wall Street strategy of value investing) is a Nash equilibrium. No market is infallible, and it’s possible that one can make money by intentionally mispricing securities. But this is only possible because other players make mistakes.

(Nash equilibrium analysis of financial markets is not some great new idea. It is standard economics. The only reason you are reading a Nash equilibrium analysis of the interaction between precious metals and official currency now on the Web, not 30 years ago in the New York Times, is that the Times gets its economics from real economists, not random bloggers, and the profession of economics today is deeply tied to the institutions that manage the global economy. Real economists do not, as a rule, spend time thinking up clever new reasons why the global financial system will inevitably collapse. They’re too busy trying to prevent it from doing so.)

What Nash equilibrium analysis tells us is that the “case B” approach is interesting, but inadequate. To look for Nash equilibria in the precious metals markets, we need to look at strategies which everyone in the economy can follow.

Let’s focus for a moment on everyone’s favorite, gold. One obvious strategy – let’s call it strategy G – is to treat only gold as savings, and to value any other good either in terms of its direct personal value to you, or how much gold it is worth.

For example, if you followed strategy G, you would not think of the dollar as worthless. You would think of it as worth 45 milligrams, because that’s how much gold you can trade one for.

What would happen if everyone in the world woke up tomorrow morning, got a cup of coffee, and decided to follow strategy G?

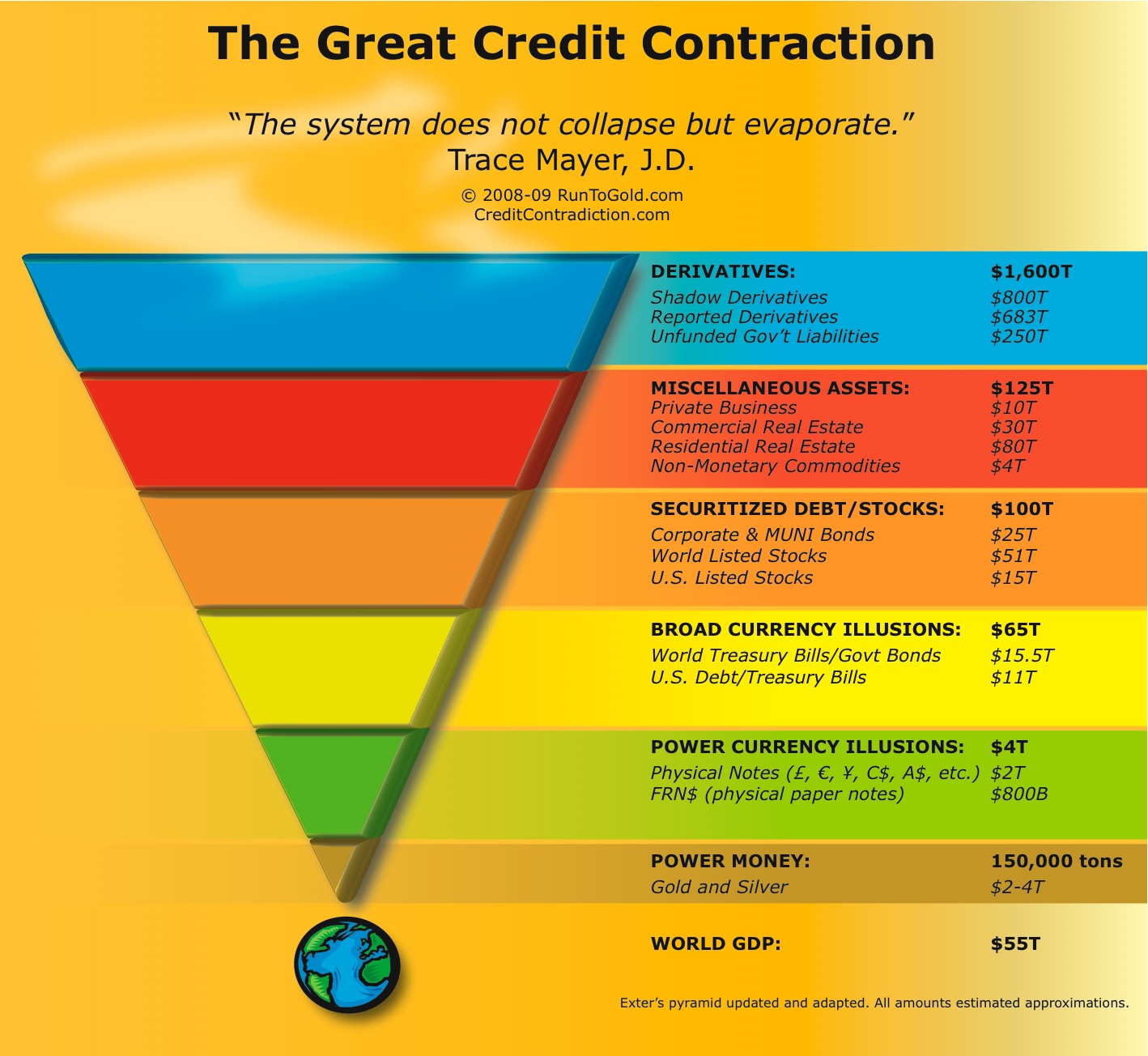

They would probably notice that at 45mg per dollar, the broad US money supply M3, at about $10 trillion, is worth about 450,000 metric tons of gold; that all the gold mined in human history is about 150,000 tons; and that official US gold reserves are 8136 tons.

They would therefore conclude that, if everyone else is following strategy G, it will be difficult for everyone to obtain 45mg of gold in exchange for each dollar they own.

Fortunately, there is no need to follow the experiment further. Of course it’s not realistic that everyone in the world would switch to strategy G on the same day.

The important question is just whether strategy G is stable. In other words, is it a realistic possibility that everyone in the world could price all their savings in gold? Is strategy G in fact a Nash equilibrium?

There are no market forces that would tend to destabilize it. Or are there? Actually, it turns out that we’ve skipped a step in our little analysis.

Levitating collectibles

The problem is that the exact same analysis works just as well for any standardized and widely available asset.

For example, let’s try it with condoms. Our benchmark of all value will be the standard white latex condom. We can have a “strategy C” in which everyone measures the worth of all their assets in terms of the number of condoms they exchange for. Cash payments will be made in secure electronic claims to allocated boxes of condoms, held in high-security condom vaults in the condom district of Zurich. And so on.

This is obviously ridiculous. But why? Why does the same analysis seem to make sense for gold, but no sense for condoms?

It’s because we’ve ignored one factor: new production.

Let’s step back for a moment and look at why people “invest” in gold in the first place. Obviously they expect its price to go up – in other words, they are speculating. But as we’ve seen, in the absence of investment the gold price would be determined only by industrial supply and demand, a fairly stable market. So why does the investment get started in the first place? Does it just somehow generate itself?

What’s happening is that the word “investment” is concealing two separate motivations for buying gold.

One is speculation – a word that has negative associations in English, but is really just the normal entrepreneurial process that stabilizes any market by pushing it toward equilibrium.

The other is saving. We can define saving as the intertemporal transfer of wealth. A person saves when she owns valuable goods now, but wishes to enjoy their value later.

The saver has to decide what good to hold for whatever time she is saving across. Of course, the duration of saving may be, and generally is, unknown.

And of course, every saver has no choice but to be a speculator. The saver always wants to maximize her savings’ value, as defined by the goods she actually intends to consume when she uses the savings. For example, if our saver is an American retiree living in Argentina, and intends to spend her savings on local products, her strategy will be to maximize the number of Argentine pesos she can trade her savings for.

Here are five points to understand about saving.

One is that since people will always want to shift value across time, there will always be saving. The level of pure entrepreneurial speculation in the world can vary arbitrarily. But saving is a human absolute.

Two is that savers need not be concerned at all with the direct personal utility of a medium of saving. Our example saver has little use for a big hunk of gold. Her plan is to exchange it for tango lessons and huge, delicious steaks.

Three is that from the saver’s perspective, there is no artificial line between “money” and “non-money.” Anything she can buy now and sell later can be used as a medium of saving. She may have to make two trades to spend her savings – for example, if our saver’s medium of saving is a house, she has to trade the house for pesos, then the pesos for goods. If she saves directly in pesos, she only has to make one trade. And clearly trading costs, as in the case of a house, may be nontrivial. But she just factors this into her model of investment performance. There is no categorical distinction.

Four is that if any asset happens to work well as a medium of saving, it may attract a flow of savings that will distort the “natural” market valuation of that asset.

Five is that since there will always be saving, there will always be at least one asset whose price it distorts.

Let’s see what happens when that asset is condoms. Suppose everyone in the world does adopt strategy C, just as in our earlier example they adopted strategy G. What will happen?

Just as we predicted with gold, there will be massive condom buying. Since condom manufacturers were not expecting their product to be used as a store of wealth, demand will vastly exceed supply. The price of condoms will skyrocket.

Strategy C looks like a self-fulfilling prophecy. Condoms will indeed become a costly and prized asset. And the first savers whose condom trades executed will see the purchasing power of their condom portfolios soar. This is a true condom boom.

Let’s call this effect – the increase in price of a good because of its use as a medium of saving – “levitation.”

Sadly, condom levitation is unsustainable. The price surge will stimulate manufacturers to action. Since there is no condom cartel – anyone can open a factory and start making condoms – the manufacturers have no hope of maintaining the levitated condom price. They will produce as many condoms as they can, as fast as possible, to cash in on the levitation premium.

Levitation, in other words, triggers inventory growth. Let’s call the inventory growth of a levitated good “debasement.” In a free condom market, debasement will counteract levitation completely. It will return the price of a condom to its cost of production (including risk-adjusted capital cost, aka profit). In the long run, there is no reason why anyone who wants condoms cannot have as many as he or she wants at production cost.

Of course, condom holders will realize quickly that their condoms are being debased. They will pull their savings out, probably well before debasement returns the price of a condom to the cost of producing one.

We can call the decrease in price of an asset due to the flow of savings out of it “delevitation.” In our example, debasement causes delevitation, but it is not the only possible cause – savings can move between assets for any number of reasons. If savers sell their condoms to buy Google stock, the effect on the condom price is exactly the same.

Because condom debasement is inevitable, and will inevitably trigger delevitation, savers have a strong incentive to abandon strategy C. This means it is not a Nash equilibrium.

The whole sad story will end in a condom glut and a condom bust. The episode will be remembered as a condom bubble. In fact, if we replace condoms with tulips, this exact sequence of events happened in Holland in 1637.

So why won’t it happen with gold?

The obvious difference is that gold is an element. Absent significant transmutation or extraterrestrial trade, the number of gold atoms on Earth is fixed. All humans can do is move them around for our own convenience – in other words, collect them. So we can call gold a “collectible.”

Because it cannot be produced, the price of a collectible is arbitrary. It is just a consequence of the prices that people who want to own it assign to it. Obviously, the collectible will end up in the hands of those who value it highest.

Since the global bullion inventory is 150,000 tons, and 2500 tons are mined every year, it is easy to do a little division and calculate a current “debasement rate” of 1.66% for gold.

But this is wrong. Gold mining is not debasement in the same sense as condom production, which does not deplete any fixed supply of potential condoms. In fact, it only takes a mild idealization of reality to eliminate gold mining entirely.

Gold is mined from specific deposits, whose extent and extraction cost geologists can estimate in advance. In financial terms, gold “in the ground” can be modeled as a call option. Ownership of X ounces of unmined gold which will cost $Y per ounce to extract is equivalent to a right to buy X ounces of bullion at $Y per ounce.

Since this ownership right can be bought and sold, just as the ownership of bullion can, why bother to actually dig the gold up? In theory, it is just as valuable sitting where it is.

In the form of stock in mining companies which own the extraction rights, unmined gold competes with bullion for savings. Because a rising gold price makes previously uneconomic deposits profitable to mine – like options becoming “in the money” – the total value of all gold on earth does increase at a faster rate than the gold price. But the effect is not extreme. 2006 USGS figures show 30,000 tons of global gold reserves. This number would certainly increase with a much higher gold price – USGS reports 90,000 tons of currently uneconomic “reserve base” – but the gold inventory increase would be nowhere near proportional to the increase in price.

In practice, modeling unmined gold as options is too simple. Gold discovery and mining is a complex and political business. The important point is that rises in the gold price, even dramatic rises, propagate freely into the price of unmined gold and do not generate substantial surges of new gold. For example, the price of gold has more than doubled since 2001, but world gold production peaked in that year.

The result is that gold can still levitate stably. Even if new savings flow into gold stops entirely, debasement will be mild. The cyclic response typical of noncollectible commodities such as sugar (or condoms), or theoretical collectibles whose sources are not in practice scarce (such as aluminum) is unlikely.

Of course, if savings flow out of gold for their own reasons, it can trigger a self-reinforcing panic. Delevitation is not to be confused with debasement. Again, it is important to remember that debasement is not the only cause of delevitation.

What we have still not explained is why gold, which is clearly already levitated, should spontaneously tend to levitate more, rather than either staying in the same place or delevitating. Just because gold can levitate doesn’t mean it will.

Money in the real world

In case it’s not obvious, what we’ve just done is to put together a logical explanation of money, using gold as an example, and using only made-up terms like “collectible” and “levitation” to avoid the trap of defining money in terms of itself.

Now let’s apply this theory to the money we use today – dollars, euros, and so on.

Today’s official money is an “artificial collectible.” Money production is limited by legal violence, not natural rarity. If in our condom example, the condom market was patrolled by a global condom mafia which got medieval with any unauthorized condom producers, it would resemble the market for official currency. No one can print Icelandic kronor in the Ukraine, Australian dollars in Pakistan, or Mexican pesos in Algeria.

It may be distasteful to hardcore libertarians, but this method of controlling the money supply is effective. There is minimal unlicensed production of new money – also known as counterfeiting.

It should also be clear from our discussion of gold that there is nothing, in principle, wrong with artificial paper money. The whole point of money is that its “real value” is irrelevant. In principle, an artificial money supply can be much more stable than a naturally restricted resource such as gold.

In practice, unfortunately, it has not worked out that way.

Artificial money is a political product. Its problems are political problems. It does no one any good to separate economic theory from political reality.

Governments have always had a bad habit of debasing their own monetary systems. Historically, every monetary system in which money creation was a state prerogative has seen debasement. Of course, no one in government is unaware that debasement causes problems, or that it does not create any real value. But it often trades off short-term solutions for long-term problems. The result is an addictive cycle that’s hard to escape.

Most governments have figured out that it’s a bad idea to just print new money and spend it. Adding new money directly to the government budget spreads it widely across the economy and drives rapid increases in consumer prices. Since government always rests on popular consent, all governments (democratic or not) are concerned with their own popularity. High consumer prices are rarely popular.

There is an English word that used to mean “debasement,” whose meaning somehow changed, during a generally unpleasant period in history, to mean “increase in consumer prices,” and has since come to mean “increase in consumer prices as measured, through a process whose opacity makes chocolate look transparent, by a nonpartisan agency whose objectivity is above any conceivable question, so of course we won’t waste our time questioning it.” The word begins with “i” and ends with “n.” Because of its interesting political history, I prefer to avoid it.

It should be clear that what determines the value of money, for a completely artificial collectible with no industrial utility, is the levitation rate: the ratio of savings demand to monetary inventory. Increasing the monetary inventory has a predictable effect on this calculation. Consumer price increases are a symptom; debasement is the problem.

Debasement is always objectively equivalent to taxation. There is no objective difference between confiscating 10% of existing dollar inventory and giving it to X, and printing 11% of existing dollar inventory and giving it to X. The only subjective difference is the inertial psychological attachment to today’s dollar prices, and this can easily be reset by renaming and redenominating the currency. Redenomination is generally used to remove embarrassing zeroes – for example, Turkey recently replaced each million old lira with one new lira – but there is no obstacle in principle to a 10% redenomination.

The advantage of debasement over confiscation is entirely in the public relations department. Debasement is the closest thing to the philosopher’s stone of government, an invisible tax. In the 20th century, governments made impressive progress toward this old dream. It is no accident that their size and power grew so dramatically as well. If we imagine John F. Kennedy having to raise taxes to fund the space program, or George W. Bush doing the same to occupy Iraq, we imagine a different world.

The immediate political problem with debasement is that it shows up in rising consumer prices, as whoever has received the new money spends it. If we think of all markets as auction markets, like EBay, it should be clear how this happens.

Debasement and investment

We haven’t even seen the most pernicious effect of debasement.

Debasement violates the whole point of money: storage of value. As such, it gives savers an incentive to find other assets to store their savings in.

In other words, debasement drives real investment. In a debasing monetary system, savers recognize that holding money is a loser. They look for other assets to buy.

The consensus among Americans today is that monetary savings instruments like passbook accounts, money market funds, or CDs are lame. The real returns are in stocks and housing. [Written in 2006]

When we debasement-adjust for M3, we see the reasons for this. Real non-monetary assets like stocks and housing are the only investments that have a chance of preserving wealth. Purely monetary savings are just losing value.

The financial and real estate industries, of course, love this. But that doesn’t mean it’s good for the rest of us.

The problem is that stocks and housing are more like condoms than they are like gold. When official currency is not a good store of store value, savings look for another outlet. Stocks and housing become slightly monetized. But the free market, though it cannot create new official currency or new gold, can create new stocks and new housing.

The result is a wave of bubbles with an unfortunate resemblance to our condom example. When stocks are extremely overvalued, as they were in 2000, one sign is a wave of dubious IPOs. When housing is overvalued, we see a rash of new condos. All this is just our old friend, debasement.

This debasement pressure answers one question we asked earlier: why should gold tend to levitate, rather than delevitate? Why is the feedback loop biased in the upward direction?

The answer is just that the same force is acting on gold as on stocks and housing. The market is searching for a new money. It will tend to increase the price of any asset that can store savings.

The difference between precious metals and stocks or housing is just our original thesis. Stocks and housing do not succeed as money. Holding all savings as stocks or housing is not a Nash equilibrium strategy. Holding savings as precious metals, as we’ve seen, is.

Presumably the market will eventually discover this. In fact, it brings us to our most interesting question: why hasn’t it already? Why are precious metals still considered an unusual, fringe investment?

The politics of money

What I’m essentially claiming is that there’s no such thing as a gold bubble.

This assertion may surprise people who remember 1980. But markets do not, in general, think. Most investors, even pros who control large pools of money, have a very weak understanding of economics. The version of economics taught in universities has been heavily influenced by political developments over the last century. And your average financial journalist understands finance about the way a cat understands astrophysics.

The result is that historically, the market has had no particular way to distinguish a managed delevitation from an inevitable bubble. Because of Volcker’s victory, and the defeat of millions of investors who bet on a dollar collapse, the financial world spent the next twenty years assuming that there was some kind of fundamental cap on the gold price, despite the lack of any logical chain of reasoning that would predict any such thing.

Even now, there is no shortage of pro-gold writers who predict gold at $1000, $2000 or $3000 an ounce, as though they had some formula, like the P/E ratio for stocks, that computed a stable equilibrium at this level. Of course, they do not. They are only expressing their intuitive feeling that gold is very, very cheap right now, and tempering it with the desire to be taken seriously.

Gold’s main weapon is one we alluded to already: a sudden, self-reinforcing, and complete collapse of the dollar. In a nutshell, the problem with the dollar is that it’s brittle. When Volcker did his thing, the US was a net creditor nation with a balance-of-payments surplus. Its financial system was relatively small and stable. And it had much more control over the economic policies of its trading partners – the political relationship between the US and China is very different from the old US/Japanese tension.

For the Fed, what is really frightening is not a high gold price, but a rapid increase in the gold price. Momentum in gold is the logical precursor to a self-sustaining gold panic. If the US federal government was a perfectly executed and utterly malevolent conspiracy to dominate the world, let’s face it. The world wouldn’t stand a chance. In reality, it’s neither. So a lot of things happen in the world that Washington doesn’t want to see happen, and that it could easily prevent. Anticipating surprises is not its strength. [1]

Holy Cannoli, Batman! I think this is the longest “snip” I’ve ever used in a post. Nine pages in Word, just for that quote. And I even edited several pages out of it, “to tighten it up!” I hope you enjoyed it.

To recap, a rising gold price is evidence of increasing investment demand, which confirms the belief of those that already invested in gold that it was a good investment. And because investment demand is over and above the relatively stable industrial supply and demand dynamic, any new investment dollars must bid gold away from its current owners. And because saving in gold is a Nash Equilibrium, the price will rise very high. And because gold is THE monetary metal with the highest monetary to industrial use ratio, it will have no reason to fall back when it reaches its top.

And, as ANOTHER said, “So many people worldwide think of it as money, it tends to dry up as the price rises.”

Stock, Flow, Supply and Demand

Let’s try a little thought experiment and see where it leads us. This might be a bit of a mind bender and a challenge for me to articulate, but what the heck, we’re already 11 pages into this thing. Why stop now?

Let’s think of all the physical gold in the world in the same terms as our price discovery markets classify the gold they hold secure for private parties. (You do know that the gold for sale does not belong to the exchanges, don’t you?) There is that gold which is “eligible” for delivery. And in our experiment this would be all the physical gold in the world. It is ALL “eligible” to be handed to someone else in exchange for something else. (The only requirement for eligibility in our thought experiment being that it is a physical object made of gold.) And then there is the gold that is actually “registered” for delivery. In our case this would be the gold that is up for sale or expected to go up soon.

So “eligible” is the “stock” and “registered” (for delivery) is the “flow,” sort of. (Yes, I know that flow would mean the gold coming out of the ground and then being used up in jewelry and electronics if gold was like other commodities, but it’s not, so get over it.)

Now what I just wrote is not entirely correct. You cannot simply compare stock to flow like that because they have different measuring units. Flow is measured in units/time and stock is just units. They do not and cannot compare. The only meaningful relationship they have is a ratio. Stock:Flow, or units/(units/time), which = time. This yields us a time value in which the flow will deplete the stock. So “our flow” is the amount of “registered” gold that actually gets delivered in exchange for something over a given time unit.

In the world as a whole, gold has the largest stock to flow ratio of any commodity, which is why it is unique. This means a very high time value for the depletion of gold stocks. In fact, it is an infinite time value since gold is not consumed, it is merely shuffled around until it ends up with those who value it most. So in our case we’ll think of flow as delivery demands actually being met with “registered” stock over a period of time. And in this view, “stock to flow” is a dynamic system that is complicated by many factors.

One complication is that, today, physical and paper gold exist as “stock” at par with each other inside the system. And the flow of paper happens prior to the flow of physical stock (on the price discovery exchanges). In other words, price is discovered in paper and then delivery comes later. Price is not discovered at the physical delivery window. In fact, whether there is any physical at that window when you finally show up with your paper depends on dynamic changes that happened earlier.

As the paper flow precedes the physical flow, the supply and demand dynamics can change very fast, perhaps even so fast as to give the impression that they traveled faster than the speed of light like atachyon, went back in time, and originated in the past! (Making them impossible to get out in front of!) As demand increases while registered gold is depleted and/or deregistered one of two things must happen. Either the price must skyrocket or the supply of paper must explode to take up the slack.

And as either of these things happen – or they both happen together – we end up with John Law’s self-sustaining Misesian regression spiral. Where today’s demand is determined by yesterday’s performance. (We can call it “the tachyon effect” if you’d like.) This applies to both physical gold and paper gold, and the feedback loop will have separate effects on these separate elements of the market. It will be the cause of the separation and the result will be a flood of paper and no registered gold to service the delivery demand portion of it.

Ultimately the stock to flow ratio of physical gold will go inverse to that of paper gold. Infinite flow demand against zero registered stock. Zero time until physical depletion, concurrent with infinite time until paper depletion. At this point the price will have to go infinite and paper supply will separate because parity will no longer exist.

And in case you haven’t noticed, we are now, apparently, at a novel stage in the game. The stage when it is becoming obvious to almost everyone that the Fed can do nothing but print more money (QE), and that it plans to do just that. I draw your attention to gold trading at $1,301 today as evidence! And regarding the Fed, what does a monkey with a hammer do? That’s right. It hurts itself.

Being at this stage in the game right now, when clarity is spreading like wildfire, we can expect a further run up in the price of paper gold. Of course the price discovery market buys and sells paper gold so a move in either direction is possible in the short run, but the general trend in gold should now be obvious, even to monkeys. And don’t forget that delivery of physical in this market is secondary, and only comes after price discovery occurs in paper.

So with this dynamic situation we find ourselves in, we should expect conflicting signals and responses in the gold market. The flow of gold should increase as demand from dollars pulls on the market. And the supply of gold bullion should be withdrawn or “deregistered” as the people holding it realize their investment belief has been confirmed.

From a demand perspective, flow should increase per the economic law of demand. And from a supply perspective, it should decrease. But how is this possible? Well, this is where price factors into the dynamics of the situation. In most commodities (and all other markets for that matter) flow would be measured in the weight of the good. “How many ounces are flowing?” But gold is a little different.

Because gold is behaving in this case primarily as a savings instrument, flow can be measured in the amount of savings being exchanged. Just like exchanging dollars for euros. In other words, to properly judge the flow we should look at the aggregate amount of wealth flowing “into” gold rather than the weight of gold changing hands. And in this view, the flow can increase with demand even as the stock is withdrawn. Price takes up the slack. It can even accommodate the shoeshine boy without threatening a top.

But there’s another element in this dynamic situation that must be considered. And that is paper gold. As I said, price discovery occurs in paper only, and delivery comes after the fact. So paper supply creation can easily absorb the pressure of increasing demand while relieving price of its “taking up the slack” burden.

However, unless the ratio of physical stock “registered” to become flow rises along with the creation of new paper gold, well, “Houston, we’ve got a problem.” And I’m talking about registered physical stock measured in weight, not value! Which is QUITE a problem!

Fortunately, to quote John Law (not the real one), there is no need to follow this challenging scenario further. Instead, we can just repeat ANOTHER’s line once again:

“Gold has always been funny in that way. So many people worldwide think of it as money, it tends to dry up as the price rises.”

In economic terms, ANOTHER was referring to gold’s price inelasticity of supply here. In other words, gold seems to violate the economic law of supply. As the price rises, the supply dries up.

But another funny thing also happens when gold “tends to dry up as the price rises.” Even more people join the “many people worldwide that think of it as money.” And this means that gold violates the economic law of demand as well, delivering a positive price elasticity of demand. In other words, gold is a Veblen good. But unlike a Rolls or the Mona Lisa, gold is divisible and fungible making it the Veblen good that puts the common man on equal footing with the Giants!

This is what FOA meant:

In this world we all need much; blessings from above,,,,, family,,,, home,,, friends and good health. But after all that, one must have currency and an enduring, tradable wealth asset that places our footing in life on equal ground with the giants around us,,,,,, gold!

And this is how and why gold WILL accommodate even the shoeshine boy without collapsing!

There is no such thing as a physical gold bubble.

So, to wrap this beleaguered post up, let’s just say that we have the distinct makings of a parity break between paper and physical gold in the works. The supply of paper gold must rise while the supply of physical is withdrawing (deregistering). The flow must also rise, at least in nominal terms, so the price will skyrocket to take up the slack. And as expanding paper competes with a rising price for the “slack taking-up” role, who do you think will win?

Could they each have their way? Could the price rise to take up the extra demand while supply contracts at the same time as easy paper dilution wins itself a lower price? Confused yet?

Well, this situation leaves us with an uncomfortable question. If the only price of gold we know today is the price of paper gold, what is going to happen to “the price of gold?” Will it skyrocket? Or will it plummet?

And if we apply the principles learned in John Law’s amazingly long piece in a logical way to this uncomfortable predicament, we’ll find ourselves at the conclusion that the true Nash Equilibrium is to take possession of physical gold. And, if you already have some, not to sell it while the price is rising OR falling (this time).

And with the supply of paper gold rising to meet demand while physical is being withdrawn, the only conclusion we can come to is that the gold buyers **IN SIZE** will have to stop buying from the price discovery marketplace because, if they do their due diligence, they’ll clearly see that subsequent physical delivery has become impossible at the present price.

So, in conclusion, the price of gold will plummet!

That’s right. At some point in the future, after the price of gold rockets upward, it will fall like a box of rocks! And right about that time you’ll see more of Robert Prechter on CNBC than you ever thought was possible.

But here’s the challenge. When the price of gold falls to $200 per ounce, try and get some physical. I’m sure that Kitco will sell you some from their pooled account. And GLD will be standing ready to sell you a share at $20. But just try to take delivery. I think you’ll find it will be impossible at that point.

And that’s why you’ve got to take delivery NOW, at the current “high” price of $1,300. Don’t wait for the dip. Oh, yeah, the big dip is definitely coming. A **BIG** “correction.” But will there be any physical available? Perhaps at $1,200 if you’re really lucky. At $200? No way.

When I look into MY crystal ball, here is how I see a future gold price chart developing (roughly, of course):

And with that, I’ll leave you with my replies to the email at the top:

My reply to email 1:

Is this an orderly bull market in paper gold or physical gold?

The bubble that “WILL come”… will it be in paper gold or physical gold?

Is there a difference between paper gold and physical gold?

Is your chart showing paper gold or physical gold?

My reply to email 2:

You may be right on stage 2. But my gut says that stage 3 is when it’s obvious everyone’s flooding into gold and the real physical **IN SIZE** decides its best move is to withdraw from delivery registration. At that point the paper market won’t be able to handle the flood.

My bet, when the shoeshine boy tells you to buy gold he’ll be talking about small gold coins only. GLD probably won’t even exist anymore. And in this unique historical case, the shoeshine boy will not be the bad omen of a bubble top mania phase, but he will instead be the amazing bell-ringer of a new era. One in which even shoeshine boys can save their surplus wealth in gold. One I like to call Freegold. Because a physical-only gold market can actually handle everyone PLUS the shoeshine boy, unlike any other market.

Sincerely,

FOFOA

[1] From Why the Global Financial System is About to Collapse

by John Law

Edited by me for length and content.

{kind=link}